Part 1 — What is Offer in Compromise and is it Right For your Client?

An offer in compromise (OIC) is an option offered by the IRS that allows a taxpayer to settle their debt for less than what is actually owed. This option is great for a taxpayer because it gives them a fresh start with the IRS, but the ultimate goal of an offer in compromise is to come to a legal agreement for payment that’s in the best interest of both the taxpayer and the IRS.

The three grounds for submitting an offer in compromise are doubt as to collectibility, doubt as to liability, and effective tax administration. We’ll discuss these in more detail in a moment, but here are the basic definitions and differences:

- Doubt as to collectibility is when the taxpayer is financially unable to pay their full tax debt.

- Doubt as to liability is when the tax debt has been assessed in error or the amount of debt assessed is incorrect.

- Effective tax administration is when the taxpayer is able to pay their debt but paying the full amount would either cause economic hardship or would be considered unfair because of exceptional circumstances.

Is Offer in Compromise Right for Your Client?

The IRS created the offer in compromise program because many taxpayers cannot pay their tax liability without causing themselves financial hardship. In 2016 alone, the IRS accepted 27,000 offers, amounting to $225.9 million. They also rejected 36,000 offers. So how do you know if offer in compromise is right for your client?

If you want to get your offer accepted by the IRS, you must demonstrate that your client cannot pay the full tax debt owed, that the tax is not actually owed, or that another unique situation applies where an offer is in the best interest of both your client and the IRS (see IRM 5.8.11.1). As a general rule, the IRS is likely to approve offers when they represent the most money the IRS can expect to collect within a reasonable time period.

In 2016 alone, the IRS accepted 27,000 offers, amounting to $225.9 million.

The first thing to look at when evaluating whether or not your client is a good fit for an OIC is the eligibility requirements. In order to be eligible for an offer in compromise, your client must:

- Have filed all tax returns

- Have received a bill for at least one tax debt included on their offer

- Make all required estimated tax payments for the current year

- Make all required federal tax deposits for the current quarter (if they are a business owner with employees)

Beyond eligibility, the IRS will consider the following when determining financial hardship of your client:

- Income

- Expenses

- Asset equity

- Lifestyle

Keep in mind, while certain qualifications and requirements are set in stone, the Revenue Officer reviewing your client’s case will look take into account all aspects of your client’s situation. Your client’s lifestyle will play a huge factor in whether or not the officer recommends them for an OIC. If you claim that your client can’t pay their full tax debt but they drive brand new Range Rover and own a $2 million house, they’re likely not a good candidate for a doubt ast to collectability OIC.

The IRS collects most of their information about your client’s financial situation using Form 433-A, but the rest of the information is gathered through investigation. If you are able to justify your client’s abnormally high cost of living due to special circumstances, the officer will take that into consideration (usually via effective tax administration). Just because your client has equity in their house or vehicle doesn’t necessarily mean the IRS expects them to sell those things to pay their debt.

However, if your client is living a high-end lifestyle and wants to make lifestyle adjustments more gradually (rather than abruptly with offer in compromise), you may want to look into installment agreements and pay particular attention to the Six-Year Rule in combination with the One-Year Rule (IRM 5.14.1.4.1).

One final thought to keep in mind in regard to your client’s ability to pay: while an offer in compromise is being reviewed (a process that can last several months), your client’s income and assets will be under ongoing review to make sure that at no point they become able to pay their tax debt.

Who Will Not Qualify for Offer in Compromise?

Many of your clients will want to try for an offer in compromise because of how significantly it can decrease the amount of tax debt they owe. However, not everyone is eligible, even if they have a large amount of debt. The IRS will not accept an offer in compromise for a taxpayer who:

- Has unfiled tax returns

- Has a history of not paying their taxes

- Has deliberately avoided tax payment

- Is a tax protester

- Is in an open bankruptcy proceeding (or has a business in an open bankruptcy proceeding)

- Has had their tax liabilities in question referred to the Department of Justice

As of March 2017, the IRS immediately returns any offer in compromise applications from taxpayers with outstanding returns.

The IRS immediately returns any offer in compromise applications from taxpayers with outstanding returns.

Additionally, the IRS will generally not accept offers from a taxpayer who can pay their debt in full or through an installment agreement.

Part 2 — Types of OIC: Doubt as to Collectibility, Doubt as to Liability, and Effective Tax Administration

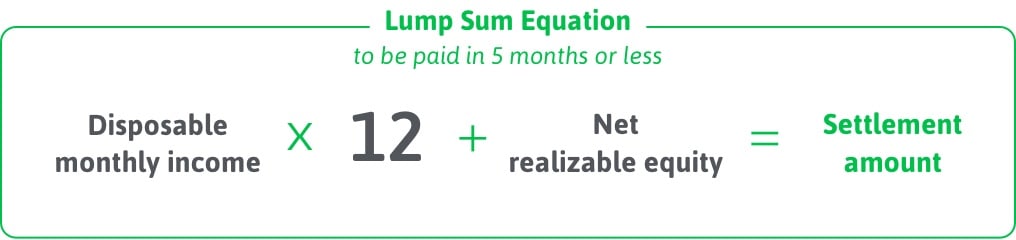

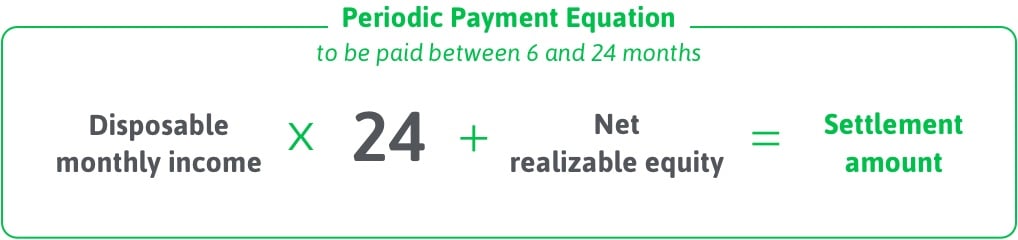

Doubt as to Collectibility: When the Taxpayer Can’t Pay

On the surface, a doubt as to collectibility offer in compromise looks fairly straightforward. The amount you offer is the product of a simple equation:

But the technical numbers that go into an OIC offer calculation are only half of the story (if you’re interested in a more technical treatment of OICs, you should check out our OIC ebook here). When the IRS considers an OIC, they don’t stop at the surface-level information you put on Form 433. They also scrutinize every piece of supporting documentation they can get their hands on—bank records, credit card statements, property valuations, medical records, and anything else that might be relevant.

The IRS goes through all of this documentation line by line looking for anything that contradicts the story your offer tells. When they do find a discrepancy, it throws up a red flag. A single discrepancy won’t necessarily sink your offer, but it does put the IRS on alert. Once a red flag pops up, they’re going to scrutinize your offer and documentation that much more, which only makes your job more difficult.

So let’s look at two examples of real cases that got flagged during my time at the IRS, and how you can help your OIC clients avoid the same mistakes.

The Case of the Mysteriously Undervalued House

I remember working one case in conjunction with the Department of Justice where the individual owed about $150,000. One of the assets they reported was a home worth $1.6 million, verified by a realtor’s valuation. However, after a little digging on our part, it became apparent that the valuation report from the realtor was incomplete. The report didn’t even list basic things like the number of bedrooms and bathroom in the home. With a little more digging, we were able to more accurately value the house at $2 million, changing the individual’s net realizable equity (NRE)—and therefore his ability to pay his taxes—substantially.

I assume that no one reading this would intentionally misreport the value of their client’s property. However, that’s not the only way a mistake like this happens. A home’s value could easily be under-reported (or even over-reported) because of a lazy or uninformed valuation by a realtor. Similarly, an online tool such as a Zillow “Zestimate” may provide inaccurate assessments in rural areas with limited market information or in markets that are fluctuating significantly.

If it is reasonable under the circumstances, your very best option is a three-step process:

- 1. Obtain a home valuation from a trusted realtor

- 2. Verify that valuation with an online tool

- 3. Submit both documents to support the numbers you put on the 433

Of course, this sort of double-documentation may not always be reasonable—or even possible. Even just a “Zestimate” can work as acceptable documentation for the value of your client’s house if the value doesn’t vary unreasonably from comparable homes in the area. Remember, your job is to convince the IRS that the numbers you put on the 433—your client’s NRE in this case—are as accurate as possible.

The Case of the Very Expensive Steaks

I worked another case as a Revenue Officer where the taxpayer claimed that they couldn’t pay their tax debt, in part, for medical reasons. The taxpayer had a cardiac condition that had led to a heart attack, and treating that condition was expensive.

On the surface, it seemed to be a compelling case. If everything was as this taxpayer claimed, the additional medical costs would have left him with little to no disposable monthly income. With no disposable monthly income, this OIC would very likely have been accepted and the taxpayer’s debt settled.

One of the mantras that was repeated often during my time at the IRS seems relevant here: the IRS isn’t a bank. They don’t fund lifestyles, they collect taxes.

Of course, there was more to the story. After going through several months’ worth of this taxpayer’s bank and credit card statements, it became clear that they had more disposable monthly income than they claimed. In fact, the statements revealed that the individual was spending about $300 per week at a high-end steakhouse.

One of the mantras that was repeated often during my time at the IRS seems relevant here: the IRS isn’t a bank. They don’t fund lifestyles, they collect taxes. In this case, the individual’s medical condition was indeed legitimate and his additional medical expenses were taken into consideration. His extravagant dining habits were not, and the offer had to be amended to a higher amount as a result.

This case is a clear illustration of how important it is to know how the IRS evaluates OIC cases. Obviously it’s hard to know exactly why tax pros make the decisions they do when preparing their offers, but I would say roughly half of all offers I recommended for rejection failed because the tax pro didn’t have a clear understanding of how the IRS evaluates offers. When you know what kind of information the IRS is looking for and where they look for it, you can arm yourself with the same information first and prepare for success.

Doubt as to Liability: When the IRS Gets It Wrong

The concept behind a doubt as to liability offer in compromise isn’t complicated: is the tax debt assessed to the taxpayer legitimate or not? If the tax has somehow been assessed in error, then a DATL offer is likely the best course of action for your client.

For instance, I remember one particular case involving a taxpayer who owned a motorcycle and ATV shop. This taxpayer had transitioned their business from a sole proprietorship to an LLC midway through the year and paid taxes accordingly. However, the IRS assessed taxes on the LLC for the entire year in an audit—essentially double dipping on taxes for 6 months. The tax had clearly been assessed in error, a perfect example of when a DATL will be effective. The tax pro submitted an offer with details showing the business transition, and the offer was accepted.

So when you’re going over a client’s case, make sure the tax was assessed correctly. Did the IRS follow all the correct procedures when assessing the tax? Did they assess the tax within the assessment statute of limitations? Maybe the IRS assessed a trust fund tax against a person who didn’t meet the criteria of willfulness or responsibility. If you can show that the IRS didn’t assess your client’s tax by the book, you can make a good case for a DATL OIC.

ETA: Good PR and Everyone’s Happy

Effective tax administration isn’t as easy to define as either doubt as to liability or doubt as to collectibility. That’s because ETA cases are the “everything else” category of the OIC world and can only be considered once DATL and DATC have been ruled out as options.

In other words, ETA is for those unique cases when the tax has been assessed correctly and the taxpayer can technically afford to pay, but there’s still a good reason why they shouldn’t.

But why would the IRS ever accept an offer if the taxpayer can afford to pay and the tax was assessed correctly?

Well first, because Congress told them to. As a part of the IRS Restructuring and Reform Act of 1998, Congress instructed the Service to consider policies that encourage taxpayers to comply with the tax laws because “they believe the laws to be fair and equitable” (IRM 5.8.11.1). Essentially, Congress believed that more people would be willing to pay their taxes if they saw that the IRS is able to make exceptions in extreme circumstances.

But also because perception matters to the IRS. They know they’re not liked—that’s an unavoidable byproduct of the job they do. They don’t want to make their perpetual PR problem worse than it already is. One piece of advice I heard often during my time at the IRS was, “Don’t do anything that would land you on the front page of the paper.” Put plainly, the IRS isn’t going to seize the house of the 90-year-old woman living on Social Security. That’s bad for everyone involved.

So that’s the driving principle behind an ETA OIC: what outcome is going to look good for everyone involved?

Let me give you another example. I worked a case involving a taxpayer who made a living running a daycare. They owed back taxes and were facing the possibility of having their home and bank accounts seized if they didn’t cooperate. Also, this taxpayer recently lost both arms, had been hospitalized for months, and was lucky to be alive. The taxpayer technically had the means to pay their tax debt. However, their offer showed clearly that, because of circumstances beyond their control, fulfilling their tax obligation would cause significant hardship.

In this case, what looks good for everyone? The taxpayer’s offer was accepted, and their IRS debt was one less thing they had to worry about.

Part 3 — Common OIC Form Mistakes (and How to Avoid Them)

During my time as a Revenue Officer at the IRS, I saw a lot of little mistakes on OIC forms that had big impacts on cases. Sometimes these mistakes would only cause confusion and stall the case until the mistake could be clarified. Sometimes the mistakes were enough to get the offer rejected outright. Either result is time-consuming and costly for both you and your clients. Let’s go over a few of these simple mistakes, why they matter, and the easiest way you can make sure they don’t happen to you.

Three Common OIC Form Problems

- 1. Bad Math

You probably wouldn’t expect this, but I saw a lot of bad math from tax pros during my time at the IRS. Not because CPAs and EAs are bad at math, but because perfectly filling out a form 433 is hard. It requires juggling dozens of complex numbers and figures, not to mention all the explanations and supporting documentation that accompany the numbers. It’s no wonder the ball gets dropped sometimes.

Unfortunately, when that ball does get dropped—a quick-sale value is calculated incorrectly, or an expense is included in the wrong calculation—the whole OIC process has to come to a screeching halt until the mistake is sorted out.

- 2. Blank Spaces

When I saw an empty field on a 433 or 656 (something I saw far too frequently), there was no way for me to know why the practitioner had left it blank. Was it blank because it didn’t apply to the taxpayer? Because they didn’t understand how to answer? Or was I missing information crucial to the case and the tax pro made a simple mistake? I had to know the answer before I could proceed with my recommendation on the offer. It’s a shame that something so small can hold up such an important decision, but I saw it happen often.

- 3. Negative Equity

This is another mistake I saw frequently: when a taxpayer’s property was worth less than they owed on it, the preparer would often subtract that negative equity from the taxpayer’s net realizable equity (NRE). You can’t do that, helpful as it may seem to your client’s case. Any asset with negative equity should have a reported equity of zero.

The Best Way to Fill Out OIC Forms

There are a couple ways you can go about making sure these kinds of mistakes don’t happen on your offers. You could hire someone to obsessively pour over every facet of your return, recalculate ever calculation and double check every form field for accuracy. You certainly don’t have time to do every offer twice.

Or you can use tax resolution software to do all that for you. I can’t speak specifically to other tax resolution softwares, but I know that Canopy solves each of the problems I’ve outlined here. When you use Canopy to prepare your OIC, our software does all of the calculating for you, make sure you don’t leave any blank fields, and helps you comply with IRS standards. Not only does that save you time, it also helps make your offer as error-free as possible. That means fewer hangups and less lost time.

Just as importantly, Canopy frees you up to worry about more important things than exactly how to comply with every nuanced IRS standard. How you spend that time—building client relationships, growing your practice, or perfecting your golf swing—is up to you.

Part 4 — What To Do If Your OIC Was Rejected

By now we’ve discussed several aspects of offer in compromise: which clients make good candidates, real reasons your client’s case would get flagged, how Canopy can help you avoid mistakes, etc. But what if your client’s offer gets rejected? What do you do then? Fortunately, you have options.

If you’re not confident that your client has good grounds for an appeal, you can look into alternative methods of tax resolution. If you still think offer in compromise is your client’s best option and you believe that you can make a strong case for acceptance, you can request an appeal.

Why Your Client’s OIC May Have Been Rejected

When we rejected an offer at the IRS, many rejections fell into a few common categories. Common reasons for rejection include the following.

Collectibility

This is the most common reason an offer is rejected. If your client’s offer is rejected on the basis of collectibility, it means the IRS views the offer amount as too low based on your client’s income and ability to pay. The IRS will use Form 433-A and other documentation to determine your client’s financial condition. Keep in mind, the IRS considers potential earning capacity when considering an offer, not just current income and financial hardship.

Additional Tax Debt

After you submit your client’s offer, your client must stay in compliance with the IRS. If they continue to accrue tax debt by not paying estimated tax payments, the IRS will assume that your client isn’t likely to comply with the potential offer in compromise. You should help keep your clients responsible and on track.

Frivolous OIC

A frivolous offer is one that is submitted solely for the purpose of delaying collection. Your client may want to buy themselves time, but the IRS will reject this type of offer immediately. As the tax professional, you need to weed these out. The IRS will know if an OIC is frivolous by red flags such as if your client shows the ability to pay a certain amount of debt but the offer is made for significantly less than that amount (without extenuating circumstances). As a Revenue Officer, I learned to quickly recognize which practitioners were responsible and which were likely to send in frivolous offers.

Additionally, while submitting an offer does delay collection, it also freezes the statute of limitations for the time the offer is being considered plus adds 30 days. It’s really not in your client’s best interest to submit a frivolous offer.

Failure to Pay

In some cases, a previously accepted OIC can be retroactively rejected due to failure to pay. If your client’s offer is accepted, they must file and pay their taxes in a timely manner for the next five years. If they do not, the OIC can be removed and the full tax debt will be reinstated.

Remember, an offer being returned is not the same thing as it being rejected. An offer is returned when the taxpayer didn’t submit necessary information, filed for bankruptcy, failed to include required application fees, hasn’t filed required returns, or hasn’t paid current tax liabilities. You can’t appeal a returned offer, but once the offer is updated it can be submitted again.

How to Request an Appeal

Now that we’ve gone over why your client’s offer may be rejected, let’s talk about what to do with a rejection. If your client’s offer is rejected, they will receive a letter from the IRS in the mail. In that letter, they will find the reason for rejection, as well as instructions for how they can appeal the decision.

Urge your clients to open any mail from the IRS immediately. The IRS will provide detailed instructions for actions going forward, but there’s a limited time frame for taking those actions. Your client must submit an appeal to the Office of Appeals within 30 days of the date on the letter.

These are the grounds for requesting an appeal as stated on the IRS website:

- You believe the IRS made an incorrect decision based on a misinterpretation of the law.

- You believe the IRS did not properly apply the law due to a misunderstanding of the facts.

- You believe the IRS is taking inappropriate collection action against your client, or your offer in compromise was denied and you disagree with that decision.

- You believe the facts used by the IRS are incorrect.

If you determine that there are grounds for an appeal, you’ll need to submit Form 13711, “Request for Appeal of Offer in Compromise.” This form should address the issues that were raised in the rejection letter, and your client will likely need to provide additional documentation.

Negotiating an Appeal

To argue any of the grounds for appeal you need to be prepared to support your position with records, evidence, and procedures. An appeal is essentially a discussion between the Appeals Officer and you on behalf of your client, and all appeals decisions are final. If you want to win an appeal you have to justify your client’s position by referencing your documentation and tying it together with the IRM, IRC, and court decisions correctly.

Keep in mind, ex parte communications are prohibited in the IRS which means an Appeals Officer cannot talk about your client’s case with the Offer Specialist who rejected it. Because of the unbiased nature of Appeals Officers, you can make your original case to them if you believe you have already included sufficient evidence. If your client’s offer was rejected based on lack of evidence, you’ll want to strengthen your case before sending it to Appeals. If you’ve already exhausted IRM and IRC references, try using case law.

Additionally, it can be effective to play to the emotional side of the argument—Appeals Officers are human after all—but it should be the “cherry on top” of your argument, not the basis. During my time at the IRS, I never lost an appeal hearing because I rooted my arguments in the IRM and IRC, and you can expect other IRS officers to do the same.

As I mentioned at the beginning of this article, the IRS rejected 36,000 offers in 2016. While the acceptance rate for offers in compromise has increased from 25 percent in 2010 to around 42 percent in 2016, there’s still a good chance your client’s offer will not be accepted. Again, the best thing to do to increase your chances of success is to be sure you can back up the foundation for your client’s case in facts and IRM references. I can’t emphasize the importance of using the IRM to support your claims enough.