The Canopy Blog

Featured Article

The Month-End Close Your Firm Deserves, Right Where You Work

Your general ledger is doing its job. Your close process shouldn’t be fighting against it. If you run bookkeeping or Client Accounting Services at your firm, you’ve probably built aContinue…

Featured Article

Canopy Coworker vs. Claude

If you had to choose between: A) a rotating series of temps who are smart and capable generalists but lack accounting expertise, or B) a fully onboarded team member whoContinue…

Featured Article

Updating Your Firm’s Brand and Messaging

Early in my career, I saw firsthand the limitations of a compliance-driven firm. So, when it came time to build my own, leading with advisory was the obvious choice. ButContinue…

Featured Article

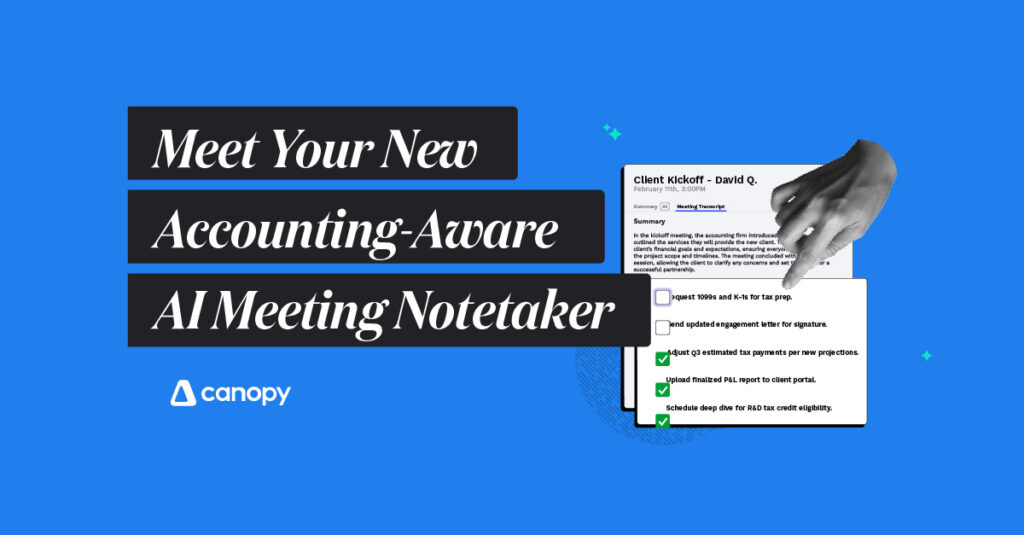

Smart Meeting Notes, Right Where They Should Be

Your meetings are working. Your notes should be too. If you’re like most modern accounting firms, you’ve probably already experimented with AI meeting assistants. Maybe you’ve tried Otter.ai to transcribeContinue…

Latest

All Posts

Accounting Firm Marketing

Accounting Technology

Advisory Services

AI

Canopy Updates

Client Management

Firm Growth

Firm Operations

PE, Mergers & Acquisitions

Practice Management

Workflows & Automations

Best Tax Practice Management Software in 2026

Jun 11, 2026

Read More

Canopy Coworker vs. Claude

May 29, 2026

Read More