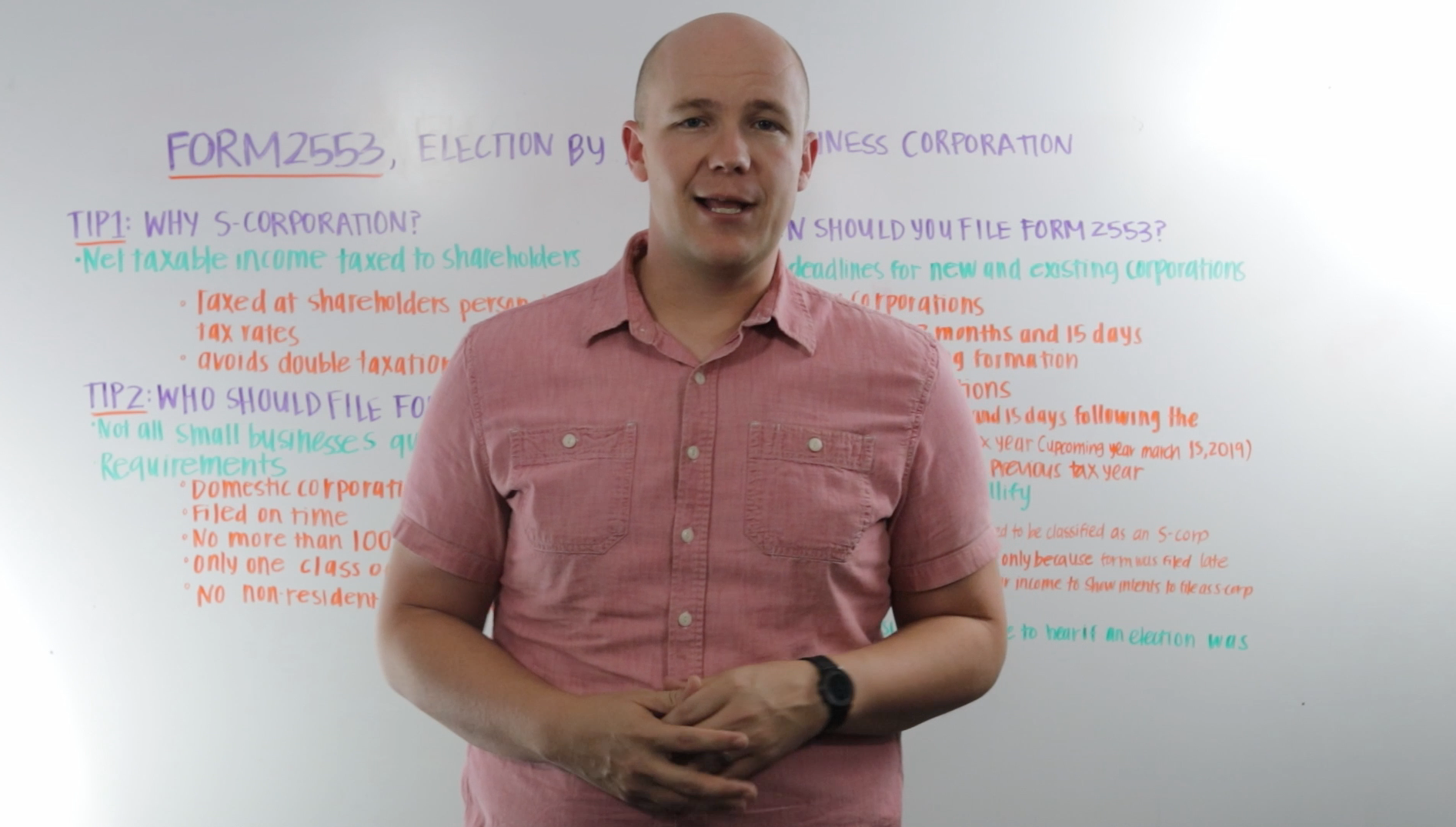

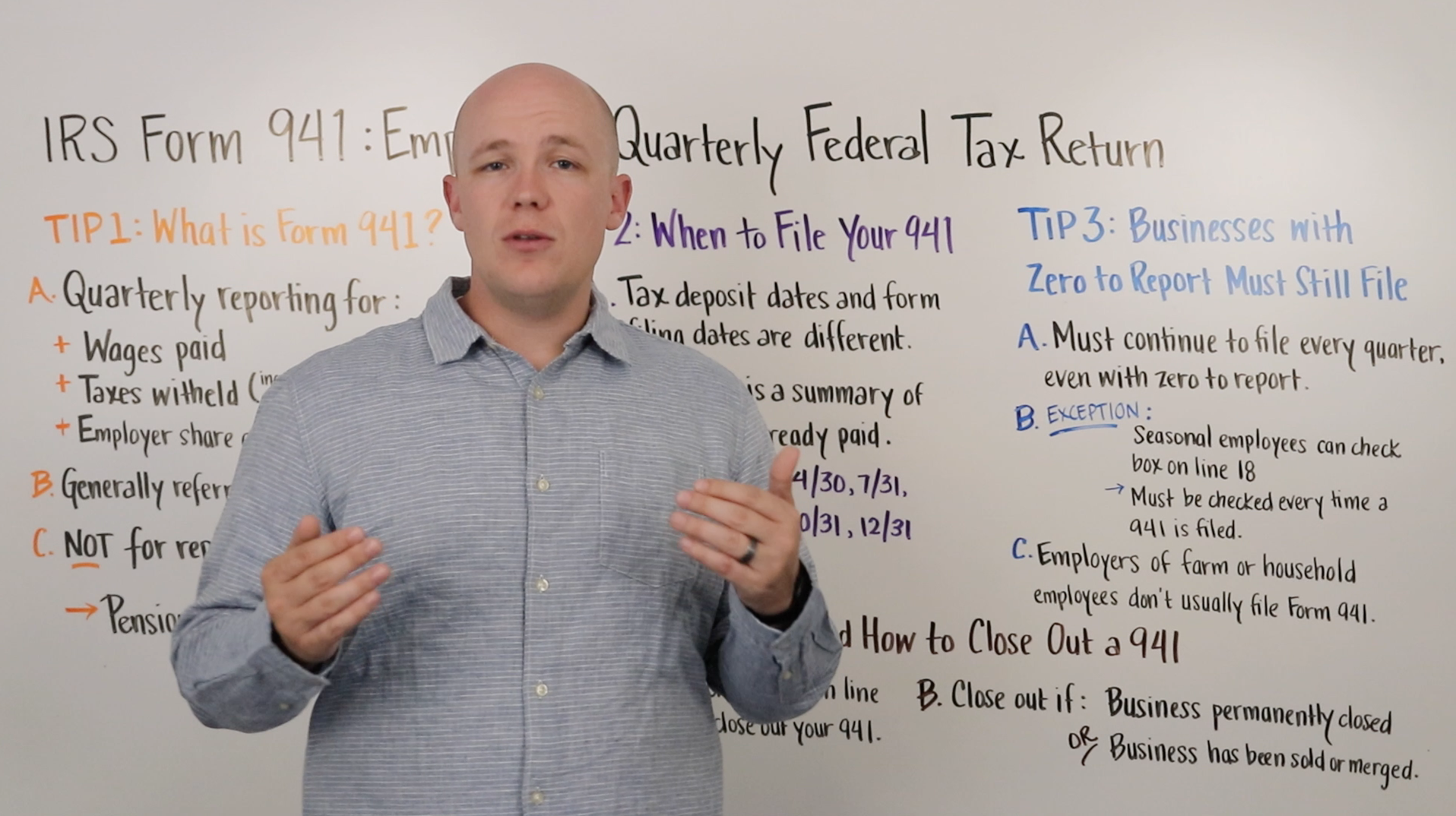

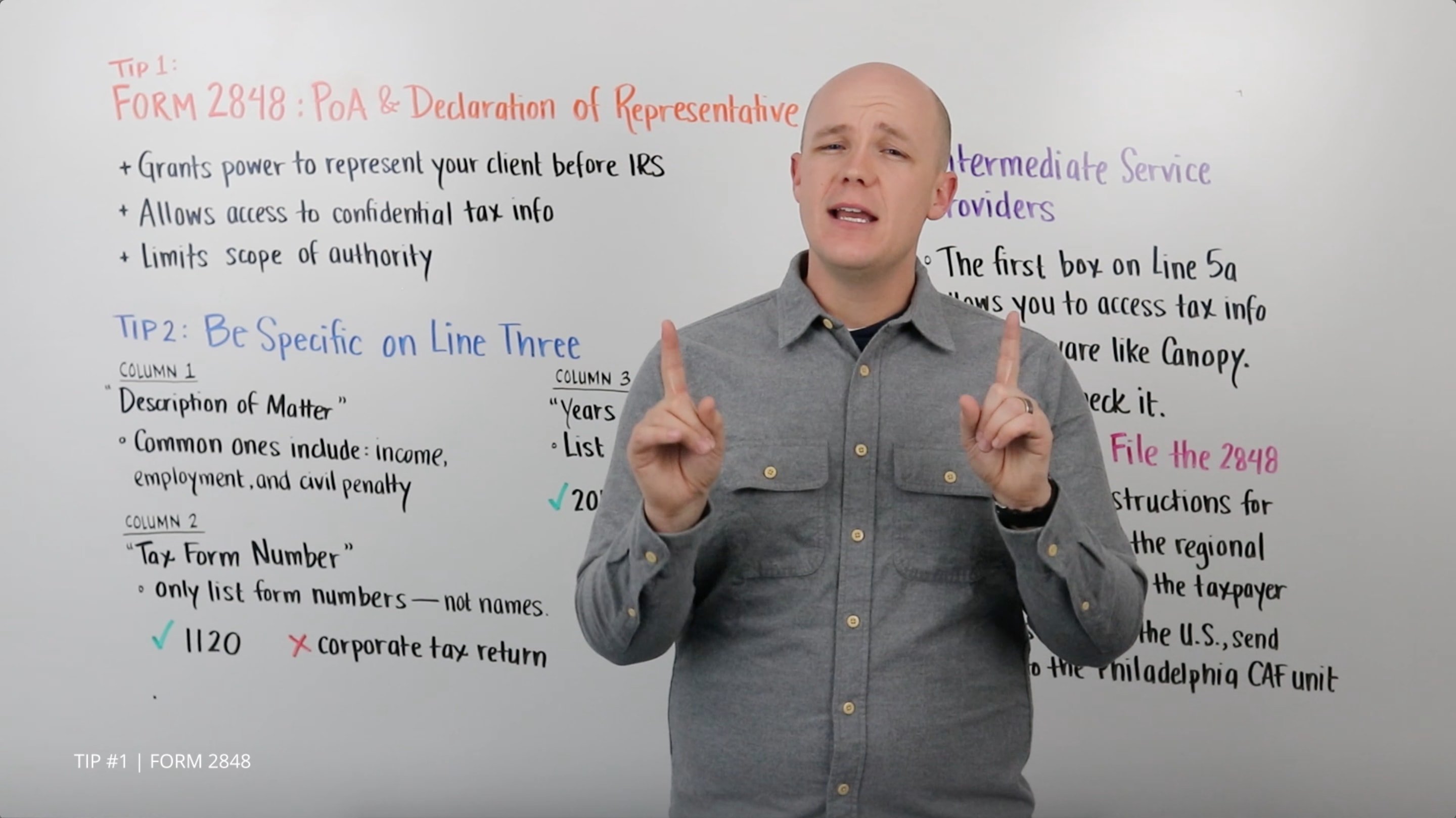

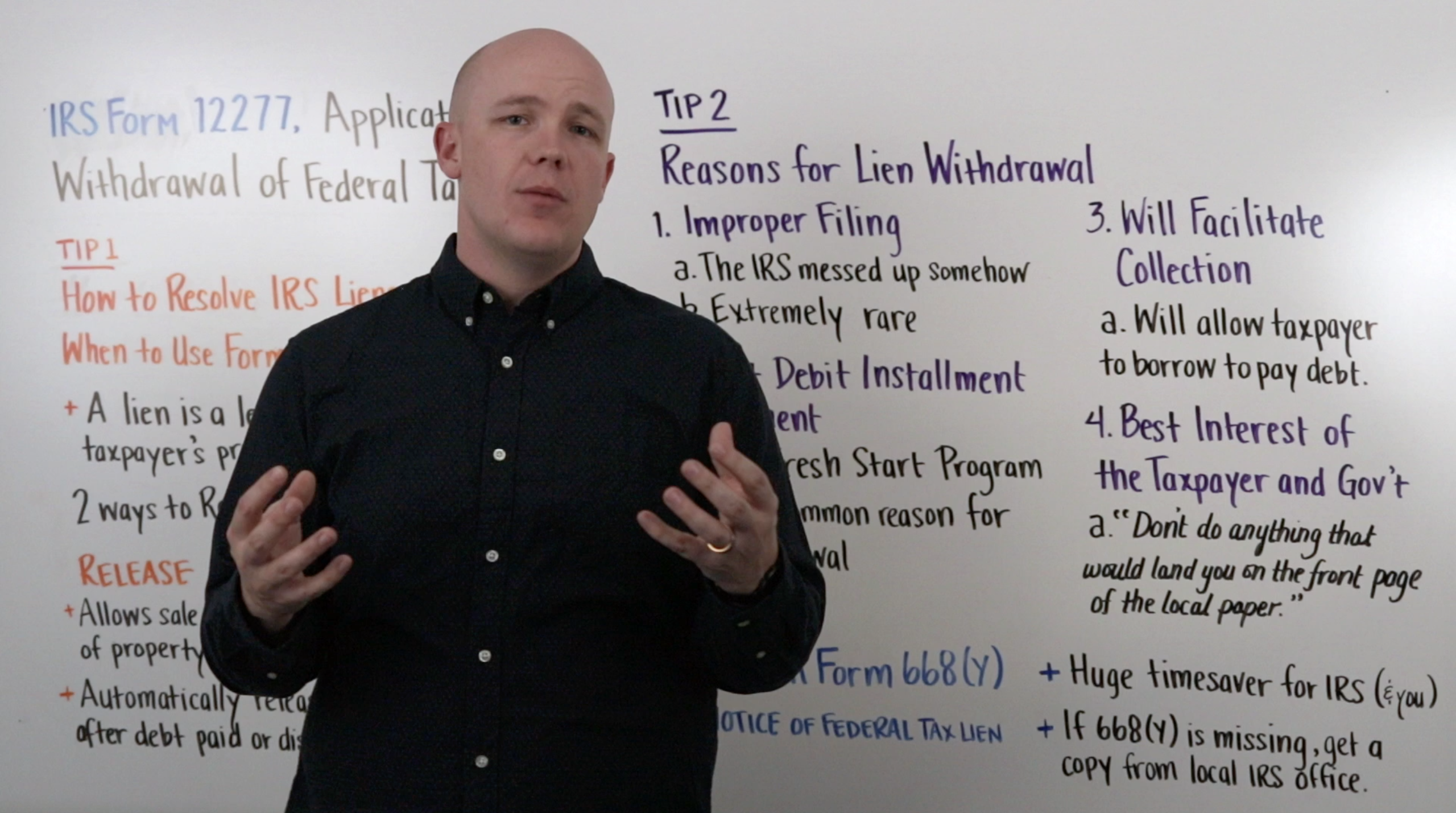

Today are talking about Form 2553, Election by a Small Business Corporation. In this video, we dive into why you would want to become an S-corporation, who should file Form 2553, and when you should file Form 2553. A corporation is considered a C-corporation by default. A corporation can file Form 2553 to make an election to become an S-corporation under section 1362(a). In order to qualify, companies must fulfill certain criteria and follow specific processes, which we will get into shortly. Let’s dive in.

Tip #1 WHY S-CORPORATIONS?

It’s important to understand why a corporation would want to become an S-corporation. Small companies typically elect to become S-corporations so that their net taxable income is taxed to the shareholders of the corporation rather than the corporation itself. This means that the small company can pass its income, credits, deductions, and losses to its shareholders for tax purposes. Income will be reported on the shareholders personal returns and taxed at their personal tax rates and not subject to any corporate taxes.

C-corporations, on the other hand, run the risk of being taxed twice: both at the corporate and shareholder level when dividends are paid out.

Tip #2 WHO SHOULD FILE FORM 2553?

With all the clear benefits, why doesn't everyone elect to become an S-corporation with Form 2553? Unfortunately, not all small business can qualify for an S-corp election.

In order to be eligible to be considered as an S-corp, a business must meet the following requirements:

- The corporation must be domestic. This means that they do most, if not all, their work within the United States

- The Form 2553 has to be filed on time.

- The corporation can have no more than 100 shareholders.

- The corporation, or eligible entity, can have only one class of stock.

- And the corporation cannot have any nonresident alien shareholders.

To see a complete list of these qualifications, check out the IRS Form 2553 instructions.

#Tip 3 WHEN SHOULD YOU FILE FORM 2553?

This is one of the most important details and often an unnecessary cause of frustration.

There are separate deadlines for Form 2553 depending on if a corporation is new or existed previously.

New companies must file an S-corp election within the first 2 months and 15 days following their initial formation. This means that within their first 75 days as a company they must file if they want the S-corp election to take effect in their first year of taxes.

For existing businesses, the S-corp election must be filed no later than 2 months and 15 days after the beginning of the tax year that the S-corp election is to take effect. For 2019, this deadline is March 15. Additionally, existing businesses can file Form 2553 any time in the tax year previous to the tax year that the S-corporation election is to take effect.

A corporation that misses the deadline must wait to file until the next tax year, which also means that they must wait until the next year for the S-corp election to take effect.

Of course, there are some cases in which the IRS is willing to offer relief for companies that missed the deadline. Companies may still be eligible to become an S-corp if they meet a series of conditions.

For example:

- The corporation clearly intended to be classified as an S-corp by the election date.

- All company shareholders reported their income according to S-corp filing requirements.

- S-corp election was not granted only because they filed their Form 2553 late.

- Or, the corporation was able to provide reasonable cause for missing the deadline.

For more information on exceptions to the deadline, check out IRS Form 2553 instructions.

Form 2553 generally takes 60 days from the submission date to hear if an election was accepted or not. If it is accepted, you will receive a notification stating that the tax status has been changed and is now an S-corporation.

Get Our Latest Updates and News by Subscribing.

Join our email list for offers, and industry leading articles and content.