In our recent Canopy webinar we dove into 3 key topics that can allow firms to make more money and scale their organizations more sustainably. There are so many ways a firm can operate with more focus and strategy, but in the recent webinar we dove into the big ways that can make fast changes.

The Dichotomy between Service and Operations.

Firm owners must manage two sides of a firm: the side that produces the revenue (the Service side), and the side that runs the firm (the Operations side). We describe this as a dichotomy because there is a healthy pull between these two parts of running a firm. This tension is always there and it helps us remember that to deliver great technical services, we also have to run our businesses well. In a sense, we can become an example to our clients of how a business should operate well.

Unfortunately, few firms are that example, but our profession can change that. The inability of technically-focused owners to focus on running their businesses has led our profession to do things that make younger professionals lack the desire to be part of our organizations. That has led to the difficulty to retain talent, the inability of creating a firm that anyone would purchase from us, and ultimately poor service to the clients that pay us.

As firm owners, we must manage the dichotomy of Service and Operations and begin to run our businesses as well as we provide our technical services.

Cash is King, Even for Firms.

Like our clients, we must be good at managing our cash. My partner and I consult with a lot of firms that are struggling to run their businesses well - one main issue we see in professional services is that firms take out all of their cash as pay for the partners. But that’s not how firms can scale. Running any business means you pay appropriate salaries to the owners and team, you save some of your money for growth, and you invest in the future. Cash is the lifeblood of an organization so it must be protected, saved, and invested wisely.

Unlike financial presentations and reviews, cash flow planning with clients is a 30, 60, 90 day forecast. We use software to do this work if we can (not spreadsheets unless the client is very small) and manage the ‘vital signs’ of the client’s organization. We are presenting the ins and outs of the flow of cash so we can see how our cash is looking over the next few months. And we do this typically in weekly meetings since cash flow is a vital sign (where financial presentations can be done monthly).

Mentioned earlier, firms need to be better examples to their clients of how to run a business. We can ask for our cash in different ways from our clients, showing them we know how important cash is as the lifeblood of our business. In the webinar we talked about 4 ways a firm can place requirements on their clients to enhance cash flow:

-

Requiring a client to go through a process of methodical onboarding means you can dictate how your relationship looks and feels, so that trust is a result.

-

Have clients agree to a price up front (called value pricing or fixed pricing) so that you can go ahead and take your cash to pay your labor, and fund your growth.

-

Ask a client to sign a 12 to 18 month agreement with your firm - this longer commitment enhances stickiness and allows you to price on a cadence (like weekly or monthly).

-

Now that you have onboarded the client, agreed to a price up front, and committed to a longer relationship, it’s easy to tell your client that drafting your prices every month is required to work with your firm.

And another thing - as firms we have to manage our own bookkeeping, cash flow reporting, and financial reporting every single month. So if the accounting for your own firm is behind, then you are not living the example our clients need us to live in front of them (and it stresses us out hoping no one will find out).

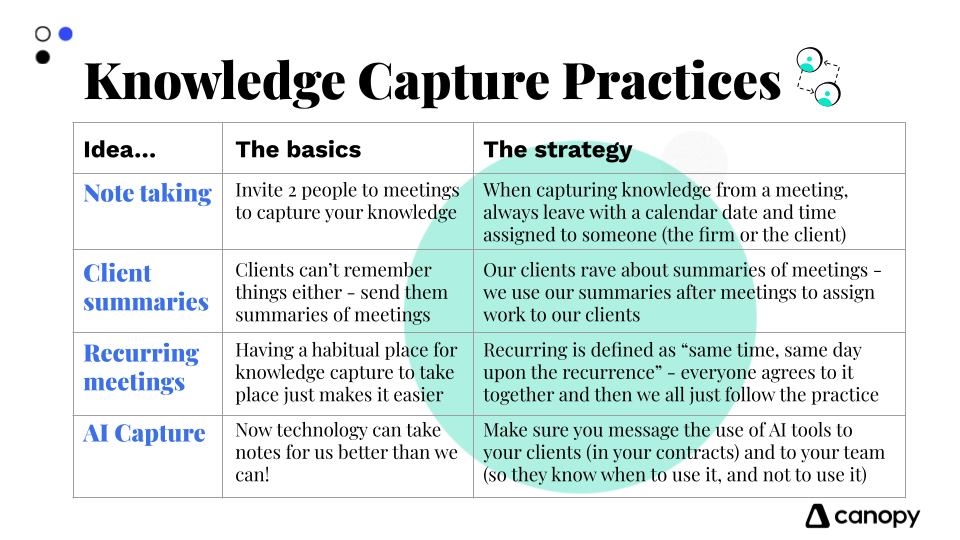

The Value of Knowledge Capture.

Knowledge is essentially the inventory of what we have to sell as professional firms. It’s our only ‘widget.’ Leveraging our minds and the minds and work of our smart team is all we have to produce a deliverable and ask to be paid for it. Then we can conclude that how we manage knowledge capture in our firms is key. What is knowledge capture? It is our processes, systems, software, and team structures that allow us to take in knowledge from clients, turn that knowledge into value, and then deliver that knowledge for a price.

Knowledge is what you sell, so how you manage it is your key to profitability (and efficiency). Managing knowledge capture helps your team to be more efficient and deliberate in their work, allowing you as the firm owner to gradually step out of direct client service. Further, maintenance of your workflow systems is your tool for proper knowledge capture and delivery of services. Too few firms manage the scope of their services or even teach their team what ‘scope’ means. You’re losing money when your team is doing work for clients that the clients aren’t paying for. Further, if team do this consistently then they are giving away part of their capacity that you will have to replace with new team members.

In our webinar we gave 4 very practical ways to manage and capture knowledge in your firm:

These ideas may all seem mundane, but they are few (of the many) ways we protect the vital asset we are selling everyday - our knowledge. Selling our knowledge for a price is something on the radar of the firm owner, not necessarily the team member. In fact, the team member doesn’t have to be fully aware of this exchange (knowledge for a price), but it does behoove the firm owner to teach these concepts to the team so that they are cognizant of the importance of their work and not giving away their knowledge.

Webinar Q&A

We had a few unanswered questions from our webinar, and I want to tackle those below.

Q: You said that your onboarding process lasts about a month. Do you ask them to enter that long-term relationship at the beginning of that process to keep them there, or at the end when they understand more of the agreement?

A: Our firm’s onboarding process usually lasts between 3 weeks to 6 weeks, depending on the start date we agree to with the potential client. Once they sign our form online, that’s when we let them know that we’ll be asking them for a long term commitment. Most clients don’t have any issues with that.

Q: What are some strengths in your firm that you feel like separates yourself from the other firms?

A: We are deeply niched in our industry. We service large digital design agencies. We’ve consulted with them for so long we know how to restructure their organizations for maximum efficiency, or help owners/partners change how they want to lead their organizations.

Q: Your firm is completely digital. Is that the direction most firms should be looking to move to? Are there any advantages left of having a physical firm?

A: Yes I think there will still be brick and mortar offices as well as virtual firms. Both have advantages and disadvantages. For example, it is more difficult to embody and maintain a great close culture in a virtual firm. You have to be extremely intentional to pull it off. On the other hand, virtual offices have the advantage to hire anyone in the world to be on their team, which is going to be a great advantage is such a difficult labor market.

Get Our Latest Updates and News by Subscribing.

Join our email list for offers, and industry leading articles and content.